China April PE market boasts intensive turnarounds – China PE market has stabilized into the threshold of Apr, and market transaction is elevating on the whole – China April PE market - Arhive

China April PE market China April PE market China April PE market China April PE market China April PE market China April PE market China April PE market China April PE market China April PE market China April PE market China April PE market

Apr PE market boasts intensive turnarounds

China PE market has stabilized into the threshold of Apr, and market transaction is elevating on the whole. After the Fresh Green holiday (Apr 5-7) in particular, market has bounced greatly, as rebound of most products offset the decline since the 2018 China Lunar New Year holiday. The robust increase is based on multiple supporting factors, which have been taken by domestic petrochemical suppliers and as a result push prices up significantly.

Prices of almost all PE products ramp up in the first half of Apr. In East China, ex-works offers of LLDPE 7050H from Sinopec Zhenhai Refinning & Chemical (ZRCC) has risen by 400yuan/mt to 9,850/mt, and traded levels are above 10,000yuan/mt. The increase is propelled by ZRCC’s turnaround schedule in late Apr. Ex-works rates of LDPE 2426H from Sinopec Maoming Petrochemical is up by 400yuan/mt to 10,000yuan/mt. All HDPE sources except for pipe-grade have been climbing vigorously, as raffia-grade 5000S of Sinopec Yangzi Petrochemical (YPC) increases 700yuan/mt to 11,400yuan/mt, and injection-grade 8008 from PetroChina Dushanzi Petrochemical up 700yuan/mt to 11,200yuan/mt.

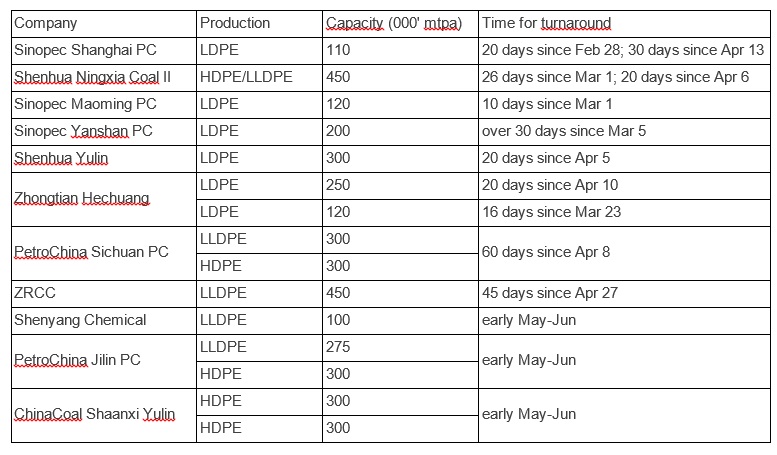

Among most supportive factors, intensive turnaround during Apr-May is the major supportive reason for the quick rise in PE market. Turnarounds have gradually laid out since end of Feb and appear mostly intensively currently. China domestic PE plant operating rate has been cut heavily to 78.64% on Apr 16, sharply down by 10% from the beginning of Apr.

Production of LDPE has been shut most intensively compared with LLDPE and HDPE, and this have directly turned market trend from a panic decline to quick elevation. LDPE plants, including Sinopec Shanghai Petrochemical, Sinopec Maoming Petrochemical, Sinopec Yanshan Petrochemical, Shenhua Yulin and Zhongtian Hechuang, etc. are gradually shut since end Feb. Notably, Sinopec Yanshan Petrochemical’s 200kt/year LDPE plant is accidentally shut on Mar 5 for technical problem and remains closed for over a month and thus largely affects market supply, and triggers bullish trend in the market. Even though some players believe LDPE stocks are still ample, market ramps up quickly.

LLDPE supply is also cut heavily. Shenhua Ningxia Coal Industry II’s 450kt/year and PetroChina Sichuan Petrochemical’s 300kt/year plant have been shut and taken away large quantities from the market in Apr. In late market, ZRCC will shut its 450kt/year plant for two months. Mentally speaking, LLDPE segment is on a strong bullish trend.

Shortage of some HDPE sources is more evident, as the size of subsegments is smaller. Except for HDPE pipe, all grades fall in short of supply, and the lift of ex-works offers from petrochemical suppliers is most evident. Price lift of HDPE raffia and injection is quickest compared with all other PE products.

On top of domestic supply reduction, import arrivals in Apr are influenced by recent adjustment on added-value tax on manufacturing industry, as the rate will be cut from 17% to 16% effective since May 1. So some Apr ordained shipment are delayed to May in order to say the 1% rate gap. It is for sure that arrivals in Apr will be thinner, and probably leaves a gap in supply-demand in traditional importers. Domestic suppliers would take this opportunity to pull up prices and reduce stocks at the same time.

Above all, intensive PE plants’ turnaround have injected high confidence to Chinese suppliers, and reducing imports in Apr would allow more space for sellers to pull up the market. And possible rising import tax on the U.S. originated LDPE amid China-US trade frictions also attracts’ speculative mood. Led by PetroChina and Sinopec groups, domestic PE suppliers are reducing their stocks and raising prices. But after this round of quick rebound, market needs a period to consolidate current height. When transaction could be maintained around this stage, market may climb higher in late market.

Related Topics