Oil price volatility surges above $100 as geopolitical tensions and refinery stress amplify inflation risks and uncertainty across global energy markets

Oil Price Trend Analysis – March 24, 2026

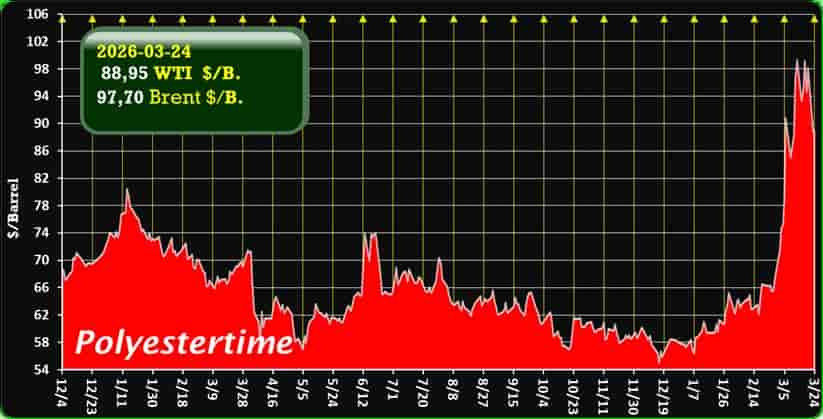

Current Oil Price Snapshot

As of March 24, 2026, the oil price remains elevated and highly volatile. Brent crude is trading in the $95–105 per barrel range, while WTI hovers between $85–95 per barrel, reflecting persistent supply concerns and geopolitical uncertainty.

| Benchmark | Price Range ($/B) | Trend | Key Driver |

|---|---|---|---|

| Brent Crude | 95 – 105 | Volatile ↑ | Geopolitical risk premium |

| WTI Crude | 85 – 95 | Volatile ↑ | U.S. supply resilience |

| Brent-WTI Spread | ~5 – 10 | Widening | Global vs domestic exposure |

Recent trading sessions show sharp swings: Brent briefly dipped below $100 before rebounding above $103, while WTI climbed back above $90 after similar volatility.

What Is Driving the Oil Price Today?

1. Geopolitical Tensions Dominate the Market

The primary driver of the oil price remains the escalating conflict involving Iran and its regional implications. Attacks on energy infrastructure and disruptions in the Strait of Hormuz—responsible for a significant share of global oil flows—have created a strong risk premium.

- Oil infrastructure damage across the Middle East continues to threaten supply

- Tanker traffic remains severely reduced

- Markets react sharply to every headline regarding escalation or diplomacy

Prices surged above $119 earlier in March before stabilizing near current levels, illustrating how sensitive the oil price is to geopolitical developments.

2. Supply Constraints and OPEC+ Strategy

OPEC+ policy is reinforcing the tightness in the oil market. The group has paused production increases, effectively limiting additional supply at a time of heightened risk.

Key dynamics include:

- Continued supply outages and logistical bottlenecks

- Strategic rerouting of Saudi exports via the Red Sea

- Strong backwardation in futures markets, signaling near-term scarcity

This combination supports elevated front-month prices, even as longer-term expectations remain more moderate.

3. Refinery Stress and Inflation Risk

A critical but often overlooked factor in the current oil price environment is refinery stress. Damage to refining capacity and logistical disruptions are tightening fuel markets, particularly diesel and gasoline.

Implications include:

- Higher refined product prices relative to crude

- Increased transportation and production costs

- Renewed inflation pressures in major economies

Central banks are already reacting. For example, expectations of further interest rate hikes are rising due to energy-driven inflation risks.

4. Demand Outlook: Resilient but Not Explosive

Global demand remains relatively stable, with growth driven mainly by non-OECD economies. However, structural factors—such as energy efficiency and EV adoption—are capping long-term demand expansion.

At the same time:

- Seasonal demand is increasing into the summer period

- Economic uncertainty is limiting upside momentum

- Demand remains strong enough to support current price levels

Investor Sentiment: Reactive and Headline-Driven

Investor sentiment in the oil market is currently highly reactive, shifting rapidly with geopolitical developments.

Recent patterns show:

- Sharp sell-offs on diplomatic news (e.g., temporary ceasefire signals)

- Immediate rebounds on renewed conflict or infrastructure attacks

- Increased speculative positioning due to uncertainty

This creates a market environment where the oil price is less driven by fundamentals alone and more by event risk and sentiment swings.

Oil Price Trends: Key Takeaways

- The oil price has risen over 35% in the past month, reflecting a strong geopolitical premium

- Brent remains more exposed to global disruptions, explaining its premium over WTI

- The market is in backwardation, indicating short-term supply tightness

Short-Term Outlook for Oil Price

Looking ahead, the oil price is likely to remain elevated and volatile in the short term.

Bullish Factors

- Continued geopolitical instability

- OPEC+ supply discipline

- Refining constraints

Bearish Factors

- Potential diplomatic resolution

- Strategic reserve releases

- Weakening global economic growth

Expected range (next 1–3 months):

| Scenario | Brent ($/B) | WTI ($/B) |

|---|---|---|

| Base Case | 90 – 110 | 80 – 100 |

| Bull Case (escalation) | 110 – 130 | 100 – 120 |

| Bear Case (de-escalation) | 75 – 90 | 65 – 80 |

What This Means for the Global Economy

The current oil price environment carries significant implications:

- Inflation risk: Higher energy costs may delay monetary easing

- Economic growth: Elevated input costs could slow industrial activity

- Energy markets: Increased volatility and tighter supply chains

- Consumers: Rising fuel and transportation costs

In essence, the oil price is once again acting as a macroeconomic shock amplifier, with ripple effects across global markets.

Final Thoughts

The oil price on March 24, 2026 reflects a market dominated by geopolitical uncertainty and structural supply constraints. While fundamentals such as demand and OPEC+ policy remain important, short-term price movements are being dictated by conflict-driven risk premiums and refinery stress.

Unless tensions ease significantly, the oil price is expected to stay elevated, keeping inflation concerns alive and reinforcing volatility across global energy markets.

More…